Insurance Analysis for High-Net-Worth Families

Request a Private Review

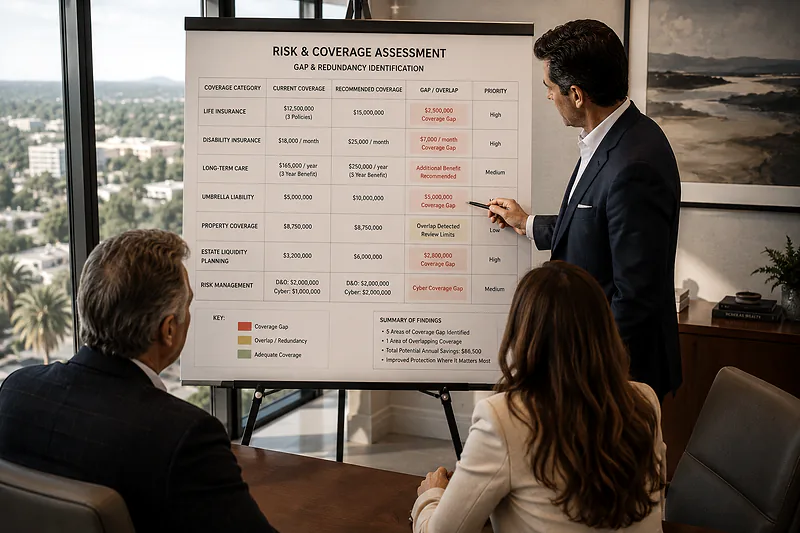

Your Insurance Portfolio Was Built for Someone

Else.

What We Analyze

1

Life Insurance Review

We audit existing policies for carrier strength, internal cost of insurance, cash value performance, and alignment with your current estate and income replacement needs.

2

Estate Liquidity Analysis

For taxable estates, we model the projected estate tax liability and determine whether existing insurance provides sufficient liquidity — or whether restructuring is needed.

3

Buy-Sell & Business Insurance

We review life and disability coverage tied to business interests, ensuring buy-sell agreements are fully funded and business continuity is protected in the event of an owner’s death or incapacitation.

4

Disability & Income Protection

High earners and business owners face significant income risk. We analyze coverage gaps, own-occupation definitions, and benefit structures to ensure your lifestyle is protected if you cannot work.

5

Long-Term Care Planning

For families with significant assets, we evaluate traditional LTC policies, hybrid life/LTC products, and self-insurance strategies — matching the right solution to your health profile and estate goals.

6

Property & Liability Coverage

High-value homes, watercraft, fine art, jewelry, and vehicles require specialized coverage. We coordinate with property and casualty specialists to ensure your physical assets and personal liability exposure are properly addressed.

67%

A Policy That Was Right Then May Be Wrong Now

A Rigorous, Conflict-Free Insurance Review

Independent Advice. No Commissions. No Conflicts.

Fiduciary Standard

Carrier Independence

Integrated Planning

Insurance Questions We Hear From South Florida Families

Most permanent life insurance policies — universal life, variable life, and whole life — have internal costs and assumptions that can drift significantly from original projections. We request an updated in-force illustration from your carrier and compare it against the original policy illustration to determine whether the policy is on track, at risk of lapsing, or underperforming. Many policies sold in the 1990s and 2000s were illustrated at interest rate assumptions that no longer hold, meaning policyholders may need to pay additional premiums or risk losing coverage entirely.

For high-net-worth families, personally owned life insurance is typically a costly mistake. Policy proceeds owned in your name are included in your taxable estate, potentially triggering estate taxes of up to 40% on the death benefit. An Irrevocable Life Insurance Trust (ILIT) removes the policy from your estate entirely, delivering the full death benefit to your heirs estate-tax-free. We review existing ownership structures and coordinate with your estate attorney to correct any misalignment.

For ultra-high-net-worth families, the purpose of life insurance shifts away from income replacement and toward estate liquidity. The goal is to provide heirs with immediate, tax-free cash to pay estate taxes, settle debts, or equalize inheritances — without forcing a fire-sale of illiquid assets like real estate, private equity, or a family business. We model your projected estate tax liability and determine the precise coverage level needed to fund that obligation.

Own-occupation disability insurance pays a benefit if you cannot perform the specific duties of your own profession — even if you are capable of working in another capacity. Any-occupation coverage only pays if you cannot work in any occupation for which you are reasonably qualified. For high-earning professionals and business owners, own-occupation coverage is the only meaningful standard. Many group disability policies are any-occupation, leaving significant income gaps for highly compensated individuals.

For families with significant net worth in South Florida, a personal umbrella policy is typically essential. Standard auto and homeowners liability limits are rarely sufficient to protect a multi-million dollar estate from a serious lawsuit. We recommend umbrella coverage calibrated to your visible wealth profile — which in Boca Raton and Palm Beach County often means $5–$10 million or more in umbrella coverage, layered above your primary policies.

Trusted by South Florida’s Most Successful Families

Nichols Wealth Partners provides independent, fiduciary-grade insurance analysis as part of a comprehensive wealth management relationship. Our clients trust us to give them the unvarnished truth about their coverage — because our only incentive is their financial wellbeing.